INTEREST RATE UPDATE – EVERYTHING YOU NEED TO KNOW!

BANK OF CANADA RATE UPDATE & MARKET OUTLOOK

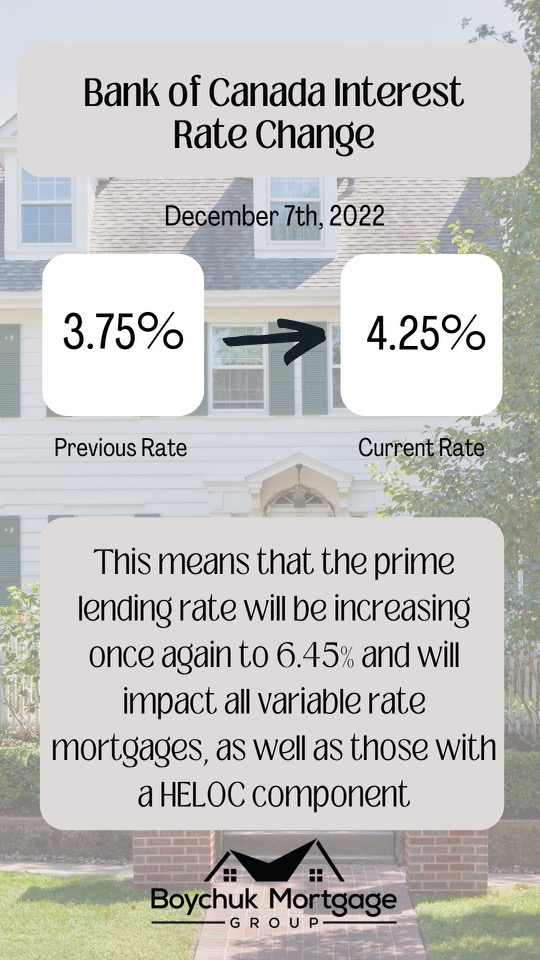

December 7th, 2022

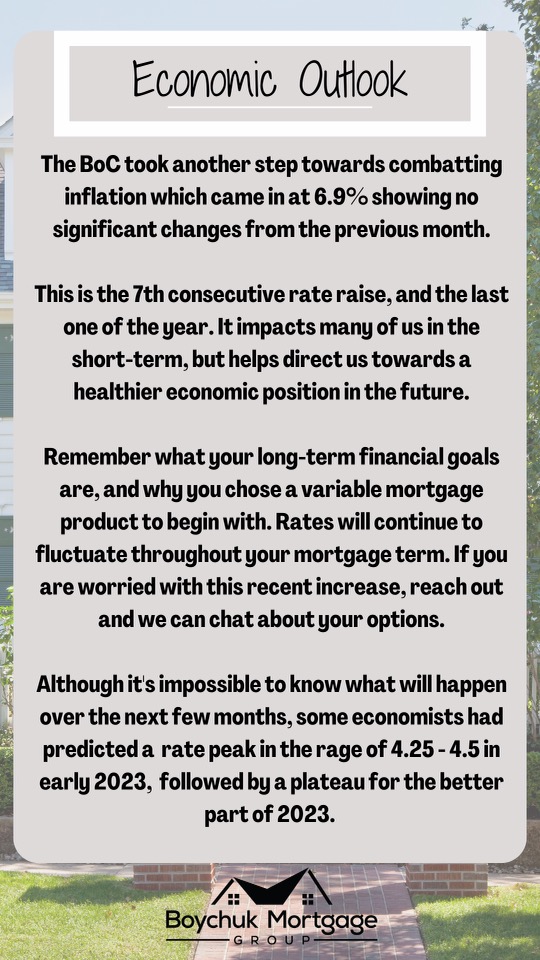

On December 7th, 2022, the Bank of Canada decided to raise their overnight policy rate once again by 50 bps. This increase brings today’s overnight rate to 4.25% and the prime lending rate to 6.45%.

While the topic can be dry and perhaps even lack excitement, we’re hopeful that we can provide you with better insight and a stronger educational foundation regarding any past and future real estate decisions.

To answer any lingering questions or concerns, we have summarized everything you need to know, including an examination of today’s market outlook, and a brief outlook on what to expect moving forward.

- So, what has Happened?

- How does this Impact You?

- Why are Interest Rates Increasing?

- Why Is a 2% Inflationary Target So Important?

- What Can We Expect Moving Forward with Interest Rates?

- What Are Your Options If You’re in a Variable Mortgage?

- Should you Lock in Now?

- Opportunities In Today’s Market?

- Economic Recap

- Some people will view this most recent policy rate hike as good news, whereas others may view this increase as bad news as it impacts their immediate finances. One positive take away is that the overnight policy rate fell short of the expected 0.75% increase, which offers insight behind the BoC’s recent decision in relation to our economic future.

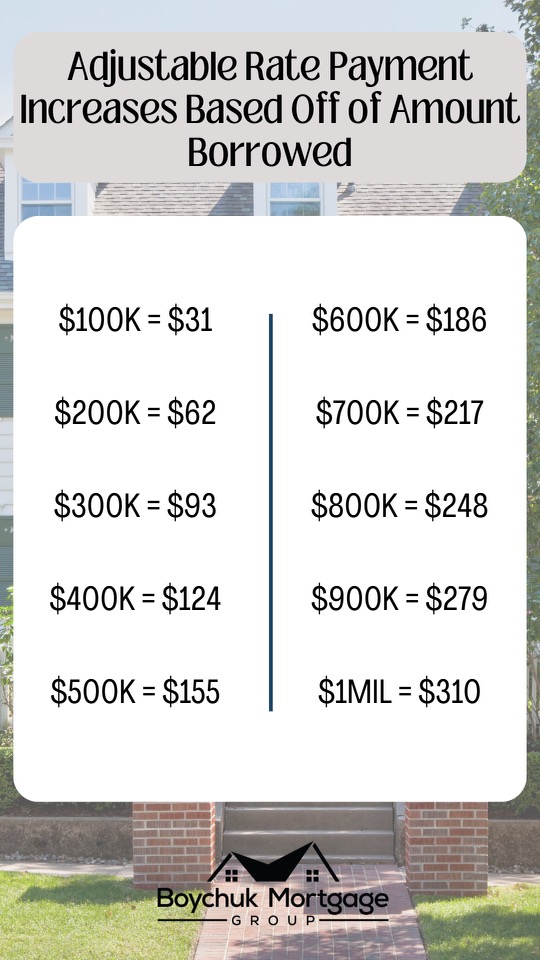

- If you are in an adjustable-rate mortgage (ARM), your variable payment will increase by about $30 for every $100,000 borrowed on your mortgage.

- If you are in a fixed rate mortgage - you will see no change.

- If you have a home equity line of credit (HELOC) - you will see an increase to your minimum interest only payment.

- If you are in a variable rate mortgage (VRM with a static payment) - your static variable payment may be close to its trigger rate and therefore trigger point.

In explanation, if you have reached your trigger rate, this means you are now making interest only payments. Therefore, to remain on track with your amortization, your options may include increasing your monthly payment, changing your payment frequency, or putting a scheduled lump sum down to stay ahead of your principal payments. You may also have the option to continue with your static payment and pay down interest only.

Click here to learn more on Variable Rates & Trigger Rates. https://www.boychukmortgages.ca/ - If you are approved but have not yet completed (funded) - you will NOT have to re-qualify. If you are in a fixed product, there is no change; whereas, if you are in a variable product, your new rate and payment will be reflected on the paperwork at the lawyer’s office.

- If you are pre-approved - your qualifying power “may” reduce depending on your pre-approval, put in place. If you have a fixed rate hold on your pre-approval, your qualifying power will remain the same, assuming your purchase completes by the rate hold expiry date. If you have a variable rate hold on your pre-approval, it is best to reach out to us so that we can confirm what your maximum borrowing power is based on the change to prime rate.

- There are various reasons as to why rates are changing, but the number one reason is no secret – Inflation!

- Let’s look at a simple example:

- A $1 cup of coffee in a 2% inflationary period, takes 36 years to double via compound interest

- A $1 cup of coffee in a 4% inflationary period, takes 18 years to double via compound interest

- A $1 cup of coffee in an 8% inflationary period, takes 9 years to double via compound interest

- Inflation compounding year over year:

- At a 2% rate of inflation, we consumers can handle that slow increase over time

- At a higher than 2% rate of inflation, we, the consumer will see the cost of every day essentials spiral beyond our financial control

- The longer inflation remains high, the harder it is to correct, posing greater risk to our economy over time.

- The real concern is the worry of inflation getting out of control, however, the unfortunate biproduct has been the increases to interest rates.

- Higher costs are especially challenging on households with FIXED incomes and is why combating inflation is so important.

- Moving forward, we can expect the BoC to very likely increase interest rates once again come their next meeting on December 7th, 2022. Economists are predicting that we will see a similar 0.50% rate increase and a potential smaller 0.25% increase in early 2023, before rates begin plateauing for the better part of 2023, and possibly decreasing come the end of 2023.

- Increase your payment

- Simply put, you will be able to increase your monthly payment by as little as 10%, up to 100%. You can do this on your online mortgage app or over the phone with your lender.

- Lock in

- With a variable rate mortgage, you will have the ability to lock in your mortgage. It’s important to remember that you will only need to lock into a fixed term that matches your current remaining term. So, for example, if you have two years remaining on your mortgage term, you will lock into the offered rate for two years.

- Restructure into a short-term fixed product (1-3 years)

- This option will give you the peace of mind, a steady payment, and the ability to capitalize on the market if rates begin to decline within your renewal date.

- Schedule lump sum payments

- Decide on a lump sum payment you are most comfortable making monthly.

- Contact your lender and schedule that monthly lump sum payment for a specified period.

- The benefits here is that you keep the flexibility within your base payment. Your payment remains at the minimum, which is helpful for future qualifications on potential investment properties or a second home.

- OR make a single lump sum payment and revisit things again later.

- Consider the HELOC option

- A big benefit to the home equity line of credit is that it only requires interest payments, ultimately creating more cash flow monthly. This option would be for those who are more concerned with monthly payments, and less concerned with paying down their principal.

- Transfer your adjustable-rate mortgage (ARM) to a static payment variable (VRM)

- While acquiring the static payment component, there is a trigger rate to ensure principal is being paid. This option allows you to know exactly what your monthly mortgage payment is going to be, while still offering the flexibility of a variable mortgage product.

- Refinance

A simple refinance may benefit you for a few reasons:

- Extending your amortization out will reduce your monthly payment

- Consolidating debt can reduce your overall monthly bills

- You can access your equity to aid in payment cushion

- We can search for more favorable lenders with lower rates

- You can add a home equity line of credit

- Ride The Wave & Weather the Storm

- It’s always important to stick to your investment strategies and remember your why. What goes up has historically always come down, so weathering today’s storm may pay dividends in your future.

Regardless of any decision, it is vital that you take a deeper look at your monthly budget and personal financial situation. Click here as we’ve provided our Monthly Budget Analysis to better help you understand what’s coming in and what’s going out - https://www.boychukmortgages.ca/

- First, ask yourself:

- Is it the monthly payment that concerns you most, or the interest?

- • If your payment concerns you most, lets discuss the static payment option (VRM mortgage)

- • If it’s the interest that concerns you most, a fixed rate is likely a higher rate, but will provide you with that certainty moving forward.

- Estimated fixed rates today:

- Insured fixed rates will range between 4.90% - 5.50%, term length dependant.

- Conventional fixed rates will range between 5.20% - 6.05%, term length dependant.

- Should you renew early if your mortgage matures in the next 12 months?

- Based on where interest rates are today and the volatility in the national economy, we recommend giving us a call to discuss your options and have us run the exact numbers to see if it makes sense for you.

- With rising interest rates, home values have dropped significantly and are inching towards further decreases following our most recent rate hike. We are also seeing a less competitive purchasing process, offering potential buyers more flexibility.

- Buyers can purchase a home today at a higher interest rate and see a SMALLER monthly payment than when compared to the same property purchased at the lower 2021 interest rates. This is because home prices have come down in value.

- You can’t change the price you pay for your home, but your mortgage rate will change many times. Over the past 30 plus years, when rates have risen, they have historically always come back down.

- REMEMBER, history has proven to show us that in inflationary periods, rates rise, and home values drop, BUT following each inflationary period is a recessionary period, in which rates drop and home values rise.

- We anticipate demand to rise substantially in the coming years with the governments promise to welcome $400,000+ new immigrants to Canada each year & continuing. With the cost to build pushing housing starts to the side lines, and our economy’s low supply in homes already prevalent, this will likely cause prices to jump once again.

- With that being said, it is always difficult to fully predict the future. However, there are many promising opportunities ahead in the next twelve months as the fundamentals of our Canadian real estate market remain strong.

Bottom Line

This will likely be the last oversized rate hike this cycle. The Governing Council next meets on January 25. Whether they raise rates will be data-dependent. If they do, it will likely be by 25 bps. Even if they pause at that meeting, it does not rule out additional moves later in the year if excess demand persists. I expect further monetary tightening, the continued bear market in equities, and a further correction in house prices.

Canadian benchmark home prices are already down nearly 10% nationwide. Several chartered banks told us this week that more than 25% of the remaining amortizations for their residential mortgages are 35 years and more. At renewal, these institutions expect to grant mortgages amortized at 25 years, which implies a substantial rise in m onthly payments. That may well be three or four years away, but clearly, many households could be pinched unless mortgage rates plunge in the interim. I do not see the policy rate falling to its pre-COVID level of 1.75% over that period because inflation back then was less than 2%, an improbable circumstance as we advance. Although supply constraints may be easing, globalization has peaked. Semiconductors produced in the US will not be as cheap, and many rents, prices, and wages will be very sticky.

Outlook from Economist - Sherry Cooper